Characteristics of Wants

- Human wants are unlimited.

- Humans wants reappear. Most wants recur. If they are satisfied once, they arise again after a certain period. We take food and our hunger is satisfied. But after a few hours, we again feel hungry, and we have to satisfy our hunger every time with food. Therefore, hunger, thirst, etc. are such wants which occur time and again.

- They compete with each other (eg pepsi v. coke)

- Wants are complementary. Wants are competitive but a few wants are complementary to each other. To satisfy one want for a good, we have to arrange for another good also. For example, the want for a car can be satisfied only when we fulfill the want for petrol also. Such wants are called complementary.

- Certain wants become habits. For example, the continuous use of opium, liquor, cigarettes, etc. become habits.

- Some wants are alternative. We can satisfy our hunger either with rice, bread, vegetables, fruit, meat, eggs, milk, etc.

- Hidden wants are those about which we do not know apparently. They lie hidden in our sub-conscious mind. But per chance, when we come across it or get satisfaction from the use of certain things, it becomes a necessity or a want for us. For example, a worker goes to his factory on foot and he does not need a bicycle. Suppose he gets a bicycle in the lottery, then he thinks that the bicycle was an important want for him.

- Certain human wants are relative to time and place. We need woollens during the winter and cotton clothes during the summer.

- All our wants are not of equal importance. Certain wants have more intensity whereas other wants have less intensity. Food, clothes and shelter are more urgent wants than radio, scooter, etc.

- Income of the individuals also affects their wants. As income increases, wants also increase. The wants of rich and poor people are not the same.

- Wants are also affected by advertisement of goods and services made by producers and sellers. When we see an advertisement about a new product in a daily newspaper or TV, there arises a want for it.

Goods & Services

Goods are items that are tangible, such as books, pens, salt, shoes, hats and folders and Services are activities provided by other people, such as doctors, lawn care workers, dentists, barbers, waiters, or online servers.

Types of Goods

Consumer goods are items people purchase to satisfy their needs and wants, such as food, shelter, and clothing. Producer goods refer to resources producers need to create goods, like cotton and steel.

Types of Services

Some types of services include educational services, communication services, transportation services and health services.

Supply and Demand

Since goods and services are scarce, their price is determined by supply and demand. Supply refers to the total amount of the goods or services that are produced, and demand refers to the total amount that consumers wish to consume.

Deductive & Inductive Approaches

There are two method of reasoning in theoretical economics. They are the deductive and inductive methods.

Deductive Method

Deduction Means reasoning or inference from the general to the particular or from the universal to the individual. The deductive method derives new conclusions from fundamental assumptions or from truth established by other methods. It involves the process of reasoning from certain laws or principles, which are assumed to be true, to the analysis of facts. Deduction involves four steps: (1) Selecting the problem. (2) The formulation of assumptions on the basis of which the problem is to be explored. (3) The formulation of hypothesis through the process of logical reasoning whereby inferences are drawn. (4) Verifying the hypothesis.

OR

Deductive economics starts with a set of axioms about economies and how they work, and relies on these principles to explain individual cases or events. Supply and demand analysis, a staple in any introductory economics course, is an example of deductive reasoning because it involves a set of generally accepted principles about demand and supply. To summarize, deduction in economics starts with a generally accepted principle and proceeds to the specific.

Inductive Method

Inductive reasoning in economics does the reverse of deductive reasoning; namely, it begins with an individual problem or question and proceeds to form a general principle based on the evidence observed in the real world of economic activity. For example, an economist who asks if a government program of public works spending will stimulate a region's economy will proceed to research the issue, collect and analyze data, and based on conclusions, form a general theory about the economic impact of fiscal policies.Need not say; when you employ inductive method in your analysis, you need to collect relevant statistical data. These statistical data serve as the basis for generalizations.

Positive & Normative Economics

Positive economics is objective and fact based, while normative economics is subjective and value based. Positive economic statements do not have to be correct, but they must be able to be tested and proved or disproved. Normative economic statements are opinion based, so they cannot be proved or disproved.

Positive

Positive statements are onjective and verifiable facts about some economic aspects whether they are true or false is immaterial. For example there is 10% unemployment is a positive statement. It maybe right or wrong but it is verifiable.

Normative

Normative economics uses valued judgements & personal opinions about what the economy should be like or what particular policy action should be recommended. It involves the question of what is good or bad.

Characteristics of Utility

1. Utility has no Ethical or Moral Significance

A commodity which satisfies any type of want, whether moral or immoral, socially desirable or undesirable, has utility, i.e., a knife has utility as a household appliance to a housewife, but it has also a utility to a killer for stabbing somebody.

2. Utility is Psychological

Utility of a commodity may differ from person to person. Psychologically, every consumer has his likes and dislikes and everyone determines his own level of satisfaction

For example:

a strictly vegetarian person has no utility for mutton or chicken.

3. Utility is always Individual and Relative.

Utility of a commodity varies in different situations in relation to time and place. Even the same consumer may derive a higher or lower utility for the same commodity at different times and different places. For example—a person may find more utility in woolen clothes during the winter than in summer or at Kashmir than at Mumbai.

4. Utility differs from usefulness-

many commodities like opium liquor, cigarettes etc. have demand because of utility, even though, they are harmful to human beings.

5.Utility cannot be Measured Objectively:

Utility being a subjective phenomenon or feeling of a consumer cannot be expressed in numerical terms. So utility cannot be measured cardinally or numerically.

6. Utility Depends on the Intensity of Want:

A want which is unsatisfied and greatly intense will imply a high utility for the commodity concerned to a person.In other words, the more of a thing we have, the less we want it.

7. Utility is Different from Pleasure:

A commodity may have utility but its consumption may not give any pleasure to the consumer, e.g., medicine or an injection. An injection or medicinal tablet gives no pleasure, but it is necessary for the patient.

Can Utility be Measured?

Utility is a psychological concept. This is different for everyone. So, it can't be measured directly. Professor Marshall has said that “Utility can be measured and its measuring rod is ‘money'. The price which we are ready to pay for an article is practically it's utility.

For example:

If I am ready to pay Rs. 1500 for a watch and Rs. 2,000 for a Radio. Then I can say that I derive utility from the watch up to the value of Rs. 1500; and from Radio up to the value of Rs. 2000.

But Prof. Hicks, Allen and Pareto have not supported Marshall’s view of measuring utility.

They are of this opinion that measuring of utility is not possible because of the following reasons:

(i) Utility is personal, psychological and abstract view which cannot be measured like goods.

(ii) Utility is different for different people. Utility is always changeable and it changes according to time and place. Therefore, it is difficult to measure such thing which are of changeable nature.

(iii) Further, measuring material ‘money is not static. Value of money always changes, therefore, correct measurement is not possible.

Kinds of Marginal Utility—Marginal utility is of three kinds:

(i) Positive Marginal Utility,

(ii) Zero Marginal Utility,

(iii) Negative Marginal Utility.

It is a matter of general experience that if a man is consuming a particular goods, then receiving of next unit of goods reduces the utilities of the goods and ultimately a situation comes when the utility given by the goods become zero and if the use of the goods still continues, then the next unit will give dis-utility. In other words it can be said that we will derive “negative utility”.

Link: http://www.economicsdiscussion.net/utility/utility-meaning-characteristics-and-types-economics/13594

Difference between stock and supply:

Stock is the quantity of output which a seller/business has with him and has not yet been brought for sale: where supply is the quantity of output brought from the existing stock of sale at a certain price in the market.

e.g. (i) stock = 1000 kg of rice

(ii) supply = 200 kg for sale at Rs. 40 per kg.

Supply is a schedule of the amount of a good that would be offered fore sale at all possible price at any period of time; e.g., a day, a week, and so on”. Acc go Meyer.

Stock means the total quantity of a commodity this exists in a market and can be offered for sale at a short notice".

The supply and stock of a commodity in the market may or may not be equal if the commodity is perishable, like vegetables, fruits, fish, etc; then the supply and stock is generally the same.

Law of Demand

Definition:

The law of demand states that other factors being constant (cetris peribus), price and quantity demand of any good and service are inversely related to each other. When the price of a product increases, the demand for the same product will fall.

Explanation

A consumer may demand one dozen oranges at $5 per dozen . He may demand two dozens when the price is $4 per dozen. A person generally buys more at a lower price. He buys less at higher price. It is not the case with one person but all people liken to buy more due to fall in price and vice versa. This is true for all commodities and under all conditions. The economists call it as law of demand. In simple words the law of demand states that other things being equal more will be demanded at lower price and lower will be demanded at higher price.

Individual Demand & Market Demand

The demand of a person is called individual demand. The demand of families and societies are called as market demands. Prince decreases, individual demand increases. The market demand is the sum of individual demand.

Why demand curve falls?

There are three reasons for it as listed below:

- (purchasing power) Income Effect : When price of a commodity falls, consumer's real income rises that is he can now purchase more of the commodity with the same income.

- Substitution effect (when the price is lowered among two choices, you choose the cheaper one and the income effect increases)

- Number of buyers increase.

Assumptions

- Income of the consumer does not change, in order to sustain the law

- The taste does not change of the buyers

- Price of related good should be same

- Population does not increase

- People do not expect early change in prices

- Quantity of money does not change

Exceptions or Exceptional Demand Curve

- Giffen good is typically an inferior product that does not have easily available substitutes, as a result of which the income effect dominates the substitution effect.Giffen goods are quite rare, to the extent that there is some debate about their actual existence.

- Hoarding

- Status Symbol A status symbol is an object which is meant to signify its owners' high social and economic standing.

A commodity which satisfies any type of want, whether moral or immoral, socially desirable or undesirable, has utility, i.e., a knife has utility as a household appliance to a housewife, but it has also a utility to a killer for stabbing somebody.

The supply and stock of a commodity in the market may or may not be equal if the commodity is perishable, like vegetables, fruits, fish, etc; then the supply and stock is generally the same.

Law of Demand

Definition:

The law of demand states that other factors being constant (cetris peribus), price and quantity demand of any good and service are inversely related to each other. When the price of a product increases, the demand for the same product will fall.

Explanation

A consumer may demand one dozen oranges at $5 per dozen . He may demand two dozens when the price is $4 per dozen. A person generally buys more at a lower price. He buys less at higher price. It is not the case with one person but all people liken to buy more due to fall in price and vice versa. This is true for all commodities and under all conditions. The economists call it as law of demand. In simple words the law of demand states that other things being equal more will be demanded at lower price and lower will be demanded at higher price.

Individual Demand & Market Demand

The demand of a person is called individual demand. The demand of families and societies are called as market demands. Prince decreases, individual demand increases. The market demand is the sum of individual demand.

Why demand curve falls?

There are three reasons for it as listed below:

- (purchasing power) Income Effect : When price of a commodity falls, consumer's real income rises that is he can now purchase more of the commodity with the same income.

- Substitution effect (when the price is lowered among two choices, you choose the cheaper one and the income effect increases)

- Number of buyers increase.

Assumptions

- Income of the consumer does not change, in order to sustain the law

- The taste does not change of the buyers

- Price of related good should be same

- Population does not increase

- People do not expect early change in prices

- Quantity of money does not change

Exceptions or Exceptional Demand Curve

- Giffen good is typically an inferior product that does not have easily available substitutes, as a result of which the income effect dominates the substitution effect.Giffen goods are quite rare, to the extent that there is some debate about their actual existence.

- Hoarding

- Status Symbol A status symbol is an object which is meant to signify its owners' high social and economic standing.

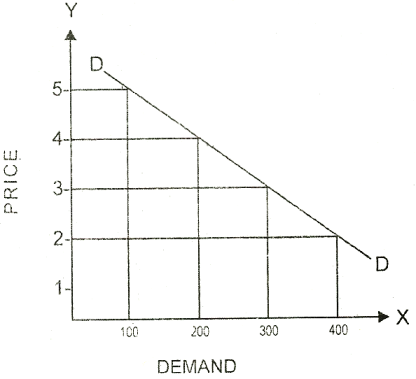

Demand schedule

Price in dollars. Demand in Kg. 5 100 4 200 3 300 2 400

The table shows the demand of all the consumers in a market. When the price decreases there is increase in demand for goods and vice versa. When price is $5 demand is 100 kilograms. When the price is $4 demand is 200 kilograms. Thus the table shows the total amount demanded by all consumers various price levels.

| Price in dollars. | Demand in Kg. |

| 5 | 100 |

| 4 | 200 |

| 3 | 300 |

| 2 | 400 |

The table shows the demand of all the consumers in a market. When the price decreases there is increase in demand for goods and vice versa. When price is $5 demand is 100 kilograms. When the price is $4 demand is 200 kilograms. Thus the table shows the total amount demanded by all consumers various price levels.

Diagram

There is same price in the market. All consumers purchase commodity according to their needs. The market demand curve is the total amount demanded by all consumers at different prices. The market demand curve slopes from left down to the right.

Indifference Curve

There is same price in the market. All consumers purchase commodity according to their needs. The market demand curve is the total amount demanded by all consumers at different prices. The market demand curve slopes from left down to the right.

Indifference Curve

Definition: An indifference curve is a graph showing combination of two goods that give the consumer equal satisfaction and utility.

OR

An indifference curve represents a series of combinations between two different economic goods, between which an individual would be theoretically indifferent regardless of which combination he received.

Each point on an indifference curve indicates that a consumer is indifferent between the two and all points give him the same utility. Indifference curves are a graphical representation of how much value an individual receives from various combinations of consumption. We measure value through the catch-all term “utility”, an concept for the value, well-being, satisfaction, benefit, etc. that someone receives.

Uses:

Used in contemporary microeconomics to demonstrate consumer preference and the limitations of a budget.

Can be useful for modeling consumer reactions to income, welfare, or wage changes (read: all labor-related) but are otherwise hard to create because most people are spending their income or time on more than 2 things.

Graph:

This is what an indifference curve looks like. Along this line, the individual in question will receive the same amount of satisfaction for any different combination of Item A and B. The slope of the indifference curve is known as the marginal rate of substitution or MRS. MRS shows the marginal utility the individual will gain (or lose) from moving up or down on the indifference curve. Marginal utility is simply the benefit the person gains from consuming an additional unit of a good. You will recall the indifference curve plots 2 different goods, so the marginal rate of substitution is telling us “how much does this person prefer good X to good Y? What is the value they get from an additional unit of this good?” The MRS is always negative for the same reason that indifference curves are convex: diminishing marginal utility.

Diminishing marginal utility

The indifference curve is convex because of diminishing marginal utility. When you have a certain number of bananas – that is all you want to eat in a week.

Understanding through tables:

Suppose all the following combinations are equivalent:

Units of Orange Units of Apple

4 1

3 2

2 3

1 4

Explanation:

Let us take the example of a consumer purchasing two goods only, apple and orange. He may prefer apple to orange but if orange becomes relatively cheap he may want to eat a few more units of it. If the price of apple becomes much cheaper he may give up orange altogether.

On the other hand, if the price of apple becomes very high he may be forced by lack of means to give up apple. Between these two extremes he will purchase both apple and orange, but will vary the proportions according to relative prices so that he obtains the advantages of small price changes of either commodity. It follows, therefore, that there are more than one combinations of apple and orange which are equally satisfactory to him.

Graphical Representation:

The our combinations are represented by small circles the figure. Apple is represented on the X- Axis, while orange is represented on the Y- Axis. The curve I1 is called an indifference curve.

Thus an indifference curve may be defined as a curve which shows combinations of goods which are equivalent to one another. It is a locus of points sharing alternative combinations of apple and orange which give the same satisfaction to the consumer. The consumer has no reason to prefer any of the combinations on the curve to any other on the same curve. He is indifferent as to which of these combinations he uses. Each indifference curve is an equal-utility curve.

Assumptions:

The indifference curve approach is based upon the following assumptions:

1. Non-Satiety: A rational person will prefer a larger quantity of a good than a smaller amount of it. It is assumed that the consumer has not yet reached the satisfaction point in respect of competition of a good.

2. Transitivity: The consumer is supposed to be consistent about his tastes and preference. For example if he prefers A to B and B to C then it follows that he also prefers A to C. This assumption is called Transitivity. 3. Diminishing Marginal Substitutability: Suppose a consumer buys orange and apple. It can be assumed that as more and more of units of apple are substituted for orange, the consumer will be willing to give up fewer and fewer units of orange for additional units of apple. As the quantity of orange consumed increases, more of it will be required to compensate for loss of apple. This follows from the principle that as the consumption of orange increases the desire for it will fall and as the consumption of apple decreases the desire for it will increase.

Therefore, the marginal rate of substitution of orange for apple increases as the quantity of orange increases relatively to apple. Alternatively we can say that the marginal rate of substitution of orange for apple diminishes as the supply of apple diminishes. This is called the Principle of Diminishing Marginal Substitutability. It is assumed that the two goods are not perfect substitutes for one another and that want for the goods are not satiable.

The Principle of Diminishing Marginal Substitutability corresponds to the older law of diminishing marginal utility.

Properties:

1. Indifference Curves Have a Negative Slope:

When the quantity of one commodity in a combination of two goods increase, the quantity of the other commodity must decline. An indifference curve must slope downwards from left to right

2.An indifference curve which lies above and to the right of another shows preferred combinations of the two commodities. This means that indifference curves with larger bundles of goods lie further up and to the right than indifference curves with smaller bundles. In general, movements from left to the right in the commodity space or on the indifference map correspond to increases in utility.

3. It cannot Intersect or Touch Another Indifference Curve

4. Indifference Curves are Convex to the Origin

Conclusion:

Thus it is concluded that:

(i) each indifference curve is a distinct line;

(ii) it slopes downwards from left to right and

(iii) it is convex to the origin.

STOCK

SUPPLY

Meaning

Stock refers to entire quantity of a commodity which is in the custody of the seller. So it is the potential supply.

Dependence

Stock depends on production.

Relationship

Stock can be greater than the supply.

(a) For perishable commodities the stock and the supply can be the same.

(b) For durable commodities, the stock can be more than the supply.

4. Order of existence

Stock comes before supply

Supply refers to the quantity of a commodity offered for sale at a given price and at a given time and place.

Supply depends on stock and price.

Supply cannot be greater than the stock.

(a) Supply is either equal or less than the stock.

Supply follow stock there cannot be supply without stock.

There is same price in the market. All consumers purchase commodity according to their needs. The market demand curve is the total amount demanded by all consumers at different prices. The market demand curve slopes from left down to the right.

Indifference Curve Definition: An indifference curve is a graph showing combination of two goods that give the consumer equal satisfaction and utility.

OR

An indifference curve represents a series of combinations between two different economic goods, between which an individual would be theoretically indifferent regardless of which combination he received.

Each point on an indifference curve indicates that a consumer is indifferent between the two and all points give him the same utility. Indifference curves are a graphical representation of how much value an individual receives from various combinations of consumption. We measure value through the catch-all term “utility”, an concept for the value, well-being, satisfaction, benefit, etc. that someone receives.

Uses:

Used in contemporary microeconomics to demonstrate consumer preference and the limitations of a budget.

Can be useful for modeling consumer reactions to income, welfare, or wage changes (read: all labor-related) but are otherwise hard to create because most people are spending their income or time on more than 2 things.

Graph:

This is what an indifference curve looks like. Along this line, the individual in question will receive the same amount of satisfaction for any different combination of Item A and B. The slope of the indifference curve is known as the marginal rate of substitution or MRS. MRS shows the marginal utility the individual will gain (or lose) from moving up or down on the indifference curve. Marginal utility is simply the benefit the person gains from consuming an additional unit of a good. You will recall the indifference curve plots 2 different goods, so the marginal rate of substitution is telling us “how much does this person prefer good X to good Y? What is the value they get from an additional unit of this good?” The MRS is always negative for the same reason that indifference curves are convex: diminishing marginal utility.

Diminishing marginal utility

The indifference curve is convex because of diminishing marginal utility. When you have a certain number of bananas – that is all you want to eat in a week.

Understanding through tables:

Suppose all the following combinations are equivalent:

Units of Orange Units of Apple

4 1

3 2

2 3

1 4

Explanation:

Let us take the example of a consumer purchasing two goods only, apple and orange. He may prefer apple to orange but if orange becomes relatively cheap he may want to eat a few more units of it. If the price of apple becomes much cheaper he may give up orange altogether.

On the other hand, if the price of apple becomes very high he may be forced by lack of means to give up apple. Between these two extremes he will purchase both apple and orange, but will vary the proportions according to relative prices so that he obtains the advantages of small price changes of either commodity. It follows, therefore, that there are more than one combinations of apple and orange which are equally satisfactory to him.

Graphical Representation:

The our combinations are represented by small circles the figure. Apple is represented on the X- Axis, while orange is represented on the Y- Axis. The curve I1 is called an indifference curve.

Thus an indifference curve may be defined as a curve which shows combinations of goods which are equivalent to one another. It is a locus of points sharing alternative combinations of apple and orange which give the same satisfaction to the consumer. The consumer has no reason to prefer any of the combinations on the curve to any other on the same curve. He is indifferent as to which of these combinations he uses. Each indifference curve is an equal-utility curve.

Assumptions:

The indifference curve approach is based upon the following assumptions:

1. Non-Satiety: A rational person will prefer a larger quantity of a good than a smaller amount of it. It is assumed that the consumer has not yet reached the satisfaction point in respect of competition of a good.

2. Transitivity: The consumer is supposed to be consistent about his tastes and preference. For example if he prefers A to B and B to C then it follows that he also prefers A to C. This assumption is called Transitivity. 3. Diminishing Marginal Substitutability: Suppose a consumer buys orange and apple. It can be assumed that as more and more of units of apple are substituted for orange, the consumer will be willing to give up fewer and fewer units of orange for additional units of apple. As the quantity of orange consumed increases, more of it will be required to compensate for loss of apple. This follows from the principle that as the consumption of orange increases the desire for it will fall and as the consumption of apple decreases the desire for it will increase.

Therefore, the marginal rate of substitution of orange for apple increases as the quantity of orange increases relatively to apple. Alternatively we can say that the marginal rate of substitution of orange for apple diminishes as the supply of apple diminishes. This is called the Principle of Diminishing Marginal Substitutability. It is assumed that the two goods are not perfect substitutes for one another and that want for the goods are not satiable.

The Principle of Diminishing Marginal Substitutability corresponds to the older law of diminishing marginal utility.

Properties:

1. Indifference Curves Have a Negative Slope:

When the quantity of one commodity in a combination of two goods increase, the quantity of the other commodity must decline. An indifference curve must slope downwards from left to right

2.An indifference curve which lies above and to the right of another shows preferred combinations of the two commodities. This means that indifference curves with larger bundles of goods lie further up and to the right than indifference curves with smaller bundles. In general, movements from left to the right in the commodity space or on the indifference map correspond to increases in utility.

3. It cannot Intersect or Touch Another Indifference Curve

4. Indifference Curves are Convex to the Origin

Conclusion:

Thus it is concluded that:

(i) each indifference curve is a distinct line;

(ii) it slopes downwards from left to right and

(iii) it is convex to the origin.

STOCK

|

SUPPLY

|

Meaning

Stock refers to entire quantity of a commodity which is in the custody of the seller. So it is the potential supply.

Dependence

Stock depends on production.

Relationship

Stock can be greater than the supply.

(a) For perishable commodities the stock and the supply can be the same.

(b) For durable commodities, the stock can be more than the supply.

4. Order of existence

Stock comes before supply

|

Supply refers to the quantity of a commodity offered for sale at a given price and at a given time and place.

Supply depends on stock and price.

Supply cannot be greater than the stock.

(a) Supply is either equal or less than the stock.

Supply follow stock there cannot be supply without stock.

|

Economic Laws

For the basis of economic laws, as early as 18th century, Adam Smith (writer of 'Wealth of

Nations') pondered over economic effects of mercantile laws. From this point

onwards, the field of Economics has put forth the leverage on its own

collection of observations and laws in an official mannerism. Economic laws

which are also known as Economic

Principles are drawn with keen interest of human nature by realizing the

human and physical nature with the aid of reasoning. But the laws of Economics

are true under certain conditions as if certain conditions have to be fulfilled

completely in order to reach the exact, authentic laws as those of physical

sciences. In the long run of life of man striving to fulfill his wants, he

follows certain principles with a regularity while engaged in the economic

activity, such set of principles are called Economic laws.

In the words of Roscoe Pound, he said,

"Law is experience developed by reason and applied continually

to further experience."

2) Productivity determines the Wage Rate. As the labors are offered wages for

working per hour, it is output per hour.

3) Reward the Producers of the commodities,

trades, goods and services and only the Producers.1 In order to flourish the society, it is important to

follow the mentioned laws. As if this third law is not followed properly the

nation maybe at brink of depression, war or various instabilities.

4) Nothing is for Free. There are no meals served for free. For example, taxes which are collected from

everyone on each and every item bought are a need of Government. Likewise, to

run an economically sound society, capital needs to be made. If this law is

violated, no profit will be made and ultimately the needs of society will not

be fulfilled. In an even generalized society there shall be no profit or loss

made by the companies and mega factories , hence all would earn the same amount

of interest. But in order to grow the economy,

variation must take place. As profit is the entrepreneurial bonus.

Likewise, there are many more laws which are made according

to the need of situation. Following are the contrasting aspects among Economic

laws and other laws.

Economic Laws Vs Physical Laws

Definition

Definition

Inconsistency

Consistency

Application

Application

DEFINITENESS

DEFINITENESS

FLEXIBILITY

FLEXIBILITY

NATURE

NATURE

ECONOMIC

LAWS VS MORAL

LAWS

DEFINITION

The Economists

of this modern age deal with the behavior, wants and needs, activities of men

in society.

DEFINITION

Laws that are

related to human conduct and originate from opinions of people are called

moral laws.

Guiding Feature

These laws teach how to regulate the economic matters of life.

Guiding Feature

These laws inspire us how to live in the society and

be accepted.

Consequences

If the laws are solely disobeyed, there are no strict retributions.

Nevertheless, one faces economic turmoil.

Consequences

In the case of transgressing moral laws of society,

there are harsh payoffs from the government and the body of politic.

Assistance

They enable us secure substantial economy.

Assistance

They help us live composedly in the human

commonality.

Nature

They are qualitative in nature.

Nature

They are also qualitative in nature.

Economic Laws Vs Social Laws

Definition

Economics

laws are generalizations about human behavior regarding monetary affairs.

Definition

Social

laws are voluntary or involuntary interactions in the human society. It

reflects on humans living together in groups, communities and the modes of

operations of this human society.

Features

o

Economic laws are universally accepted.

Features

o

Social laws are of contrasting nature among

societies.

Such

as

The

law of demand states that the quantity

demanded for goods rises as the price falls, with all other things staying

the same.2

Such

as

The

apprehension for consumption of alcohol in a Islamic society as Pakistan.

Economics

Law Vs

State Law

Definition

An

economic law is a statement of a scientific truth about human behavior

regarding fiscal matters.

Definition

State statutes, regulations, and principles and

rules having the force of law.4

Characteristics

Characteristics

o

State laws are codified and regulated.

Such

as:

The

law of demand states that the quantity

demanded for goods rises as the price falls, with all other things staying

the same.2

Such

as:

Suppose

a state declares theft is a crime. Anyone who breaks this law will be

punished by the state through law enforcement agencies.

Law of Supply

The law of supply is the microeconomic law that states that, all other factors being equal, as the price of a good or service increases, the quantity of goods or services that suppliers offer will increase, and vice versa.

For the basis of economic laws, as early as 18th century, Adam Smith (writer of 'Wealth of

Nations') pondered over economic effects of mercantile laws. From this point

onwards, the field of Economics has put forth the leverage on its own

collection of observations and laws in an official mannerism. Economic laws

which are also known as Economic

Principles are drawn with keen interest of human nature by realizing the

human and physical nature with the aid of reasoning. But the laws of Economics

are true under certain conditions as if certain conditions have to be fulfilled

completely in order to reach the exact, authentic laws as those of physical

sciences. In the long run of life of man striving to fulfill his wants, he

follows certain principles with a regularity while engaged in the economic

activity, such set of principles are called Economic laws.

In the words of Roscoe Pound, he said,

"Law is experience developed by reason and applied continually

to further experience."

Following are the top fundamental laws of economics:

1) The more the production of commodities,

trades, goods and services. The more will be value of money. In order to sustain prosperity in society

and also to increase the level of competency among other nations, this is one

of the most basic laws. The production of goods, services and etc must continue

onwards to increase the value of money. The rate of production should always be higher

than consumption.

2) Productivity determines the Wage Rate. As the labors are offered wages for

working per hour, it is output per hour.

3) Reward the Producers of the commodities,

trades, goods and services and only the Producers.1 In order to flourish the society, it is important to

follow the mentioned laws. As if this third law is not followed properly the

nation maybe at brink of depression, war or various instabilities.

4) Nothing is for Free. There are no meals served for free. For example, taxes which are collected from

everyone on each and every item bought are a need of Government. Likewise, to

run an economically sound society, capital needs to be made. If this law is

violated, no profit will be made and ultimately the needs of society will not

be fulfilled. In an even generalized society there shall be no profit or loss

made by the companies and mega factories , hence all would earn the same amount

of interest. But in order to grow the economy,

variation must take place. As profit is the entrepreneurial bonus.

Likewise, there are many more laws which are made according

to the need of situation. Following are the contrasting aspects among Economic

laws and other laws.

Economic Laws Vs Physical Laws

Definition

The Economists of this modern age deal with

the behavior, wants and needs, activities of men in society.

|

Definition

The

Natural sciences (physical laws) deal with various scientific theories and

proved experiments regarding atoms, molecules, etc.

|

|

Inconsistency

These laws are not consistent, as the human

nature is bound to differ from one another in certain ways. Hence there are

no exact laws in this field of studies.

|

Consistency

These laws are consistent, as the nature of atoms,

molecules and their behavior through many experiments has been exact and

authentically constant.

|

|

Application

Can be applied on average

conditions.

|

Application

Are true under all related conditions.

|

|

DEFINITENESS

economic laws are not 100%

exactly true.

|

DEFINITENESS

Physical laws are 100% true and can be

applied under all conditions.

|

|

FLEXIBILITY

Economic laws are

flexible.

|

FLEXIBILITY

Physical laws are not flexible.

|

|

NATURE

Economic laws cannot be

stated quantitatively. e.g. we cannot

say that 20% rise in price will cause 40% fall in demand/sale. we always say

that both are inversely proportional to each other.

|

NATURE

Physical laws can be stated quantitatively.

e.g. Avogadro's law states that 1 mole of a substance contains 6.022x1023

particles.

|

|

ECONOMIC

LAWS VS MORAL

LAWS

DEFINITION

The Economists

of this modern age deal with the behavior, wants and needs, activities of men

in society.

|

DEFINITION

Laws that are

related to human conduct and originate from opinions of people are called

moral laws.

|

Guiding Feature

These laws teach how to regulate the economic matters of life.

|

Guiding Feature

These laws inspire us how to live in the society and

be accepted.

|

Consequences

If the laws are solely disobeyed, there are no strict retributions.

Nevertheless, one faces economic turmoil.

|

Consequences

In the case of transgressing moral laws of society,

there are harsh payoffs from the government and the body of politic.

|

Assistance

They enable us secure substantial economy.

|

Assistance

They help us live composedly in the human

commonality.

|

Nature

They are qualitative in nature.

|

Nature

They are also qualitative in nature.

|

Economic Laws Vs Social Laws

Definition

Economics

laws are generalizations about human behavior regarding monetary affairs.

|

Definition

Social

laws are voluntary or involuntary interactions in the human society. It

reflects on humans living together in groups, communities and the modes of

operations of this human society.

|

Features

o

Economic laws are universally accepted.

o

These laws relate to financial facets of

human life.

o

Economic laws have an impact only on the

fiscal vista of Human society.

|

Features

o

Social laws are of contrasting nature among

societies.

o

Social laws are not universally accepted.

o

Every aspect of human life, along with

economic relations are affected by Social laws.

|

Such

as

The

law of demand states that the quantity

demanded for goods rises as the price falls, with all other things staying

the same.2

|

Such

as

The

apprehension for consumption of alcohol in a Islamic society as Pakistan.

|

Economics

Law Vs

State Law

Definition

An

economic law is a statement of a scientific truth about human behavior

regarding fiscal matters.

|

Definition

State statutes, regulations, and principles and

rules having the force of law.4

|

Characteristics

o

Economic laws are identified according to

the needs of moments.

o

Economic laws are indifferent in the makeup.

o

Economic laws are not sanctioned by the

politic body of a country rather they take their course as an outcome of free

will of the people according to the needs.

|

Characteristics

o

State laws are codified and regulated.

o

They can be good or bad in their

constitution.

o

State laws are backed by the body politic

of a government and are enforced with force and authority to properly and

justly govern a society.

|

Such

as:

The

law of demand states that the quantity

demanded for goods rises as the price falls, with all other things staying

the same.2

|

Such

as:

Suppose

a state declares theft is a crime. Anyone who breaks this law will be

punished by the state through law enforcement agencies.

|

Law of Supply

The law of supply is the microeconomic law that states that, all other factors being equal, as the price of a good or service increases, the quantity of goods or services that suppliers offer will increase, and vice versa.

No comments:

Post a Comment